13F and Form 4: Why Smart-Money Filings Work Better as Counterevidence

Executive Summary

13F and Form 4 filings are tempting public datasets. Institutional managers disclose quarterly holdings. Corporate insiders disclose trades. Both look like maps of informed capital. Both are easy to misuse.

The better conclusion is that these filings are more useful as counterevidence than as actions to copy. A stock held by many long-horizon managers may have entered a certain institutional taste profile. A stock almost absent from that peer set raises a different question: why are so many professional observers staying away? The signal is not simply that somebody filed something. The signal is in structure, concentration, delay, and absence.

Two Filing Types, Two Time Problems

Form 13F is a quarterly holdings disclosure filed by qualifying institutional investment managers, generally within 45 days after quarter-end. It covers certain long holdings. It is not a complete portfolio. It usually omits the full short book, derivatives, real-time changes, and position intent.

Form 4 is a corporate insider transaction disclosure, generally filed within two business days after the transaction. It is faster than 13F, but it is still not instantaneous. The path from transaction to filing to data aggregation to market interpretation creates multiple layers of delay.

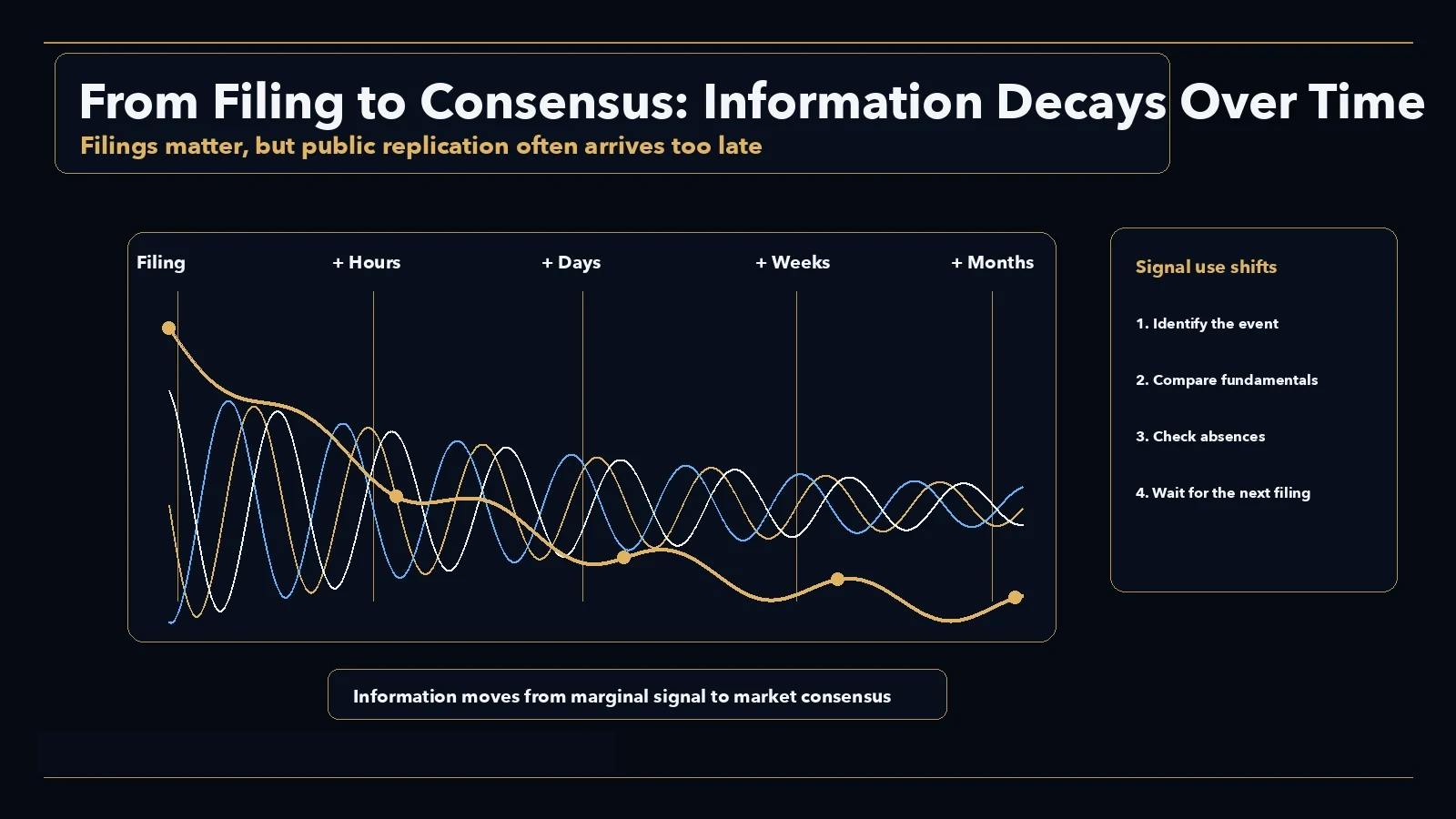

Both filings are therefore partial snapshots. A 13F is a lagged quarterly view. A Form 4 is a faster event record that the market may already be processing.

Why the Signal Decays

Early insider-trading literature did find abnormal returns, especially for opportunistic rather than routine insider trades. Cohen, Malloy, and Pomorski’s 2012 split between routine and opportunistic trades remains one of the important methodological anchors in the field.

The problem is crowding. SEC data are machine-readable. Institutions and algorithms process disclosures quickly. Media and aggregator sites accelerate diffusion. A public signal watched by more participants should have less remaining value by the time it reaches a broad audience.

That does not make the filings useless. It changes the use case. Treating a filing as something to replicate usually overstates copyability. Treating it as a question about why a behavior occurred, who is absent, and whether the filing structure conflicts with the fundamental thesis can still be useful.

The Common 13F Error: Count Is Not Consensus

13F aggregators often show how many well-known managers hold a given stock. That number can mislead. Twelve holders do not necessarily mean twelve independent high-conviction views. One large fund may account for most of the disclosed value while others hold small satellite positions.

The more useful variables are: the top holder’s share of total disclosed value, the position’s weight inside each manager’s own portfolio, the style diversity of holders, and whether the holder base has expanded or contracted over several quarters.

If one or two managers account for most of the disclosed value, the signal is concentrated exposure rather than broad consensus. If multiple managers with different styles hold the name at meaningful weights across several quarters, the signal quality improves.

Absence Can Matter More Than Presence

Public 13F data can be more useful as a falsification layer because absence is often more stable than appearance. In the June 28, 2026 public 13F aggregation snapshot used here, the sample included 83 managers. NVDA appeared in 19 manager portfolios, AMD in 5, INTC in 5, and MU in 2.

Those counts do not imply any directional conclusion on the companies. They show that institutional taste differs sharply even within the semiconductor universe. NVDA has become broadly acceptable to this manager sample. A cyclical memory name like MU is much less widely held.

For research, absence is not a veto. It is a question generator. If a thesis runs against the disclosed behavior of most comparable managers, the thesis needs to explain why: cyclicality, governance, balance-sheet quality, valuation, liquidity, or style bias. That question is more useful than the headline that one manager changed a position.

Where Form 4 Belongs

Form 4 is closer to event data, but it is still not a conclusion. Insiders may trade because of tax planning, compensation, liquidity needs, automatic plans, or personal asset allocation. Not every filing expresses a view on intrinsic value.

More informative Form 4 signals usually require several filters at once: the transaction is large relative to the insider’s history, multiple insiders act in the same direction, the trade is not merely a mechanical plan, the company is in a disputed valuation or fundamental regime, and later company disclosures do not contradict the interpretation.

Even then, Form 4 is a research entrance, not a research endpoint. Its value is to ask whether there may be a change in internal confidence or information asymmetry. The work still has to return to business quality, cash flow, competitive position, and valuation.

A Better Framework

First, treat filings as delayed data. For 13F, start with the quarter end and filing date. For Form 4, start with the transaction date and filing date. Delay is part of the evidence.

Second, decompose presence into weight, concentration, and style. A 0.2% portfolio position and a 12% portfolio position should not be counted as equal signals.

Third, treat absence as counterevidence. If a thesis looks strong while comparable long-horizon managers are mostly absent, the absence needs an explanation.

Fourth, do not treat aggregator current-price columns as primary data. Ticker changes, splits, mergers, and mapping errors can pollute displayed prices. Prices and returns need independent verification.

What We Do Not Know

13F does not show the complete portfolio and does not show real-time change. Form 4 is timelier but can still be absorbed quickly by markets. This article does not re-estimate insider-trading alpha and does not interpret any single filing as a directional claim.

The better research workflow is to put 13F and Form 4 inside an evidence stack: first build the fundamental thesis, then use filings for cross-checking or counterevidence. Running the process backward turns a filing into a story too easily.

Data and Sources

Sources are public web materials. The public 13F aggregation snapshot covers 83 managers as of June 28, 2026. Coverage is limited to the public aggregation sample, not all institutional holdings.

This report is independent KSINQ market research and personal commentary for informational purposes only. It does not constitute investment advice. Data snapshot: June 28, 2026; rewrite date: July 2, 2026.